The profitability of independent films is a complicated topic for a whole variety of reasons.

The profitability of independent films is a complicated topic for a whole variety of reasons.

The indie film sector is:

- Decentralised. It relies on a constantly shifting chain of third parties across the world, with no requirement to report to a centralised body, no third party verification and lacks even agreed reporting standards.

- Opaque. Some revenue streams withhold all data (such as VOD subscription platforms like Netflix and Amazon) while even the most transparent streams come with levels of uncertainty (i.e. theatrical gross is clear but the costs it took to earn that gross is not). But it’s not just the sources of income; distributors, sales agents and producers keep their figures extremely close to their chest, often not even sharing full data with those who have made the films they represent.

- Sometimes shady. A minority of parties are dishonest, or at very least, deliberately misleading. Over-representing revenues can make you look more successful, under-representing may reduce the need to payout profit shares and few choose to be frank about the money they have spent to make or distribute a movie.

I can’t think of any other industry which requires so much money to be spent while offering so little public data on what works.

This leaves independent filmmakers in a tricky position. An essential document for anyone trying to raise film finance is a business plan but the lack of even basic top-level information makes this an extremely hard document to write credibly.

There are two ways to tackle this information drought:

- Find a few comparisons. Many filmmakers find a few recent films similar to their own (known as ‘comps) and do all they can to track down data on how those comparisons performed.

- Understand the market. Look at how the whole market works and the kinds of films which make money. Use this data to improve your film and prove that it has a much better than average chance of succeeding.

And it’s on that second point I can help today.

Over the past year or so I have been working on an investigation of profitability within the independent film sector, covering all films made worldwide over the past two decades. Using real-world data (public and private) together with modelling likely outcomes from common practices, I have been able to find patterns in the dark noise of film financial data.

I’m going to share a few of the headline findings here to help frame expectations for filmmakers and investors looking to put their money into the independent film sector.

I am also going to start doing some training events around the world to share the details with filmmakers in a live environment. I have thought hard about the best way to share the findings and decided that it needed to be live courses. No amount of blog posts can contain all the data, no book can stay up to date and no online course can adapt to the audience’s unique needs.

I’ll be in New York on Saturday 19th October 2019 and in London on Saturday 23rd November 2019. Next year I’ll be travelling far further to reach more filmmakers (contact me if your organisation can host a course)

In the meantime, here is a sense of the profitability of independent films. I warn you now – it’s not pretty…

How many independent films recoup their investment?

The level of specificity we can bring to this question depends on how narrow we make our inclusion criteria. If we want to know about all films ever made then a large degree of modelling and projection is required, whereas picking a single movie lets us get to a much more specific answer.

The level of specificity we can bring to this question depends on how narrow we make our inclusion criteria. If we want to know about all films ever made then a large degree of modelling and projection is required, whereas picking a single movie lets us get to a much more specific answer.

Let’s focus on films made in the United States, as we can then use whether or not they reached US cinemas as a strong indicator of their performance. Mix that in with other data, and we can produce a fairly reliable picture of sector profitability.

Note: This is looking at films intended for theatrical release, thereby excluding TV movies and straight-to-video productions, such as gems like Little Mermaid 2 and Transmorphers. The data on these films is much harder to assess at scale and they wouldn’t fall into many people’s idea of a “film” (more on this at the end of the article).

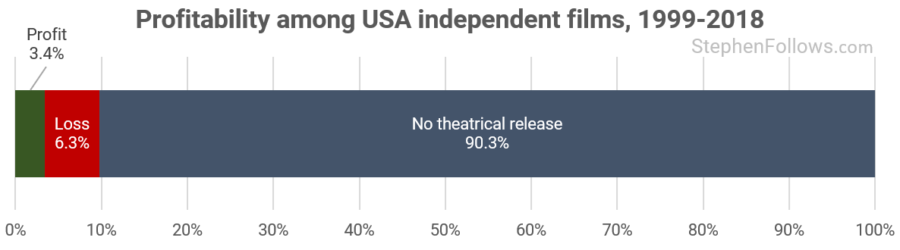

Over the past two decades (1999-2018) I found 37,472 feature films made in the US. Only 5.7% were made or released by one of the six five major Hollywood Studios, meaning that 94.3% were independent films.

Nine out of ten didn’t get a theatrical release (i.e. were shown in commercial cinemas) and are therefore statistically very unlikely to be profitable. It is possible that one or two had other significant sources of income (See Notes for more details) but for the vast majority of films, it’s extremely likely that they were loss-making.

Of those which did reach cinemas, the majority did not earn enough to recoup the costs of making, marketing and distributing the movie.

If we were to randomly select an independent film made in the US over the past twenty years, there is a 3.4% chance it was a profitable investment for its backers. Just slightly better than one in thirty.

However, this is an artificial situation as that assumes true random selection. In the real world, there are all sorts of data points an investor can take into account when weighing up an investment.

How do independent films compare to films from Hollywood Studios?

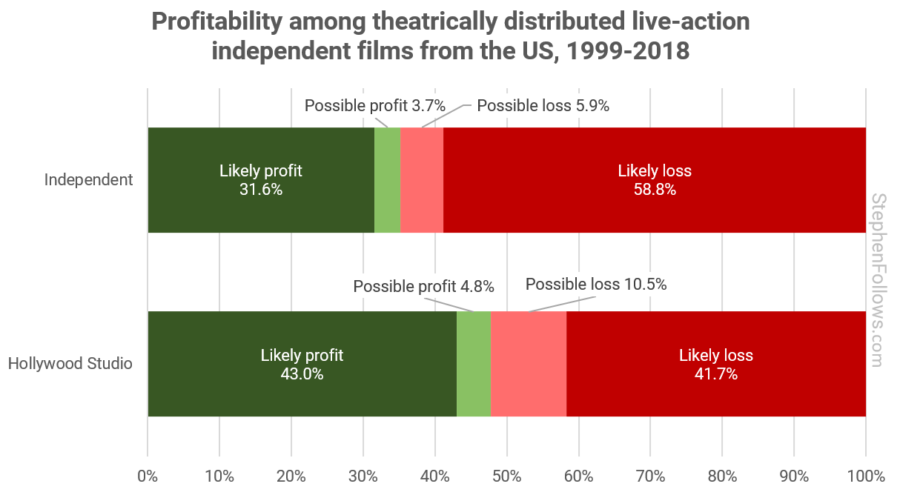

Let’s take a closer look at the profitability rates of those released in cinemas. In that select group, we can be confident that just under a third were profitable, almost 60% did not recoup their costs and the rest sit somewhere in the middle.

Unsurprisingly, Studio films have a much better rate of profitability. And yet, with all their money, power, contacts, experience, distribution channels and famous names, we could be forgiven for expecting that they would fare better than 50:50. The film world is indeed a strange one!

What types of independent films make money?

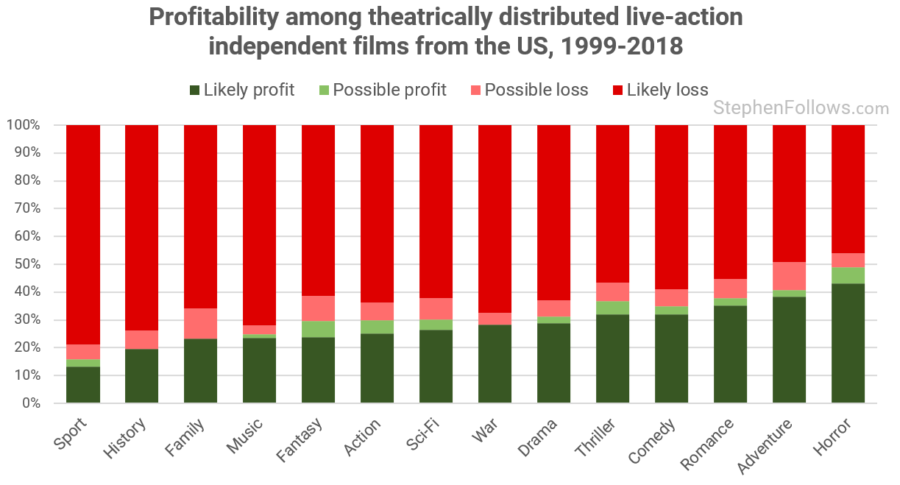

Finally, let’s sub-divide this group again, this time by genre.

Independent horror films which reached cinemas ever-so-slightly outperform Hollywood movies in profitability, although still with just under 50% breaking even.

The poorest performing genres are sports movies and historical films with recoupment rates of around 16% and 20% respectively.

Learn more

These are just the headlines of a huge research project I have been conducting. The truth is that there is a lot filmmakers can do to increase their chances of reaching profitability, and there are signals investors can spot to help them maximise their chance of recouping.

It’s not as simple as a five-point plan (otherwise I’d have included it here!) but I have built a day-long course to go over what I have found.

If you’re in either New York (19 October) or London (23 November), come join me at one of my upcoming live courses. It’s an intensive day exploring what data can reveal about how the independent film world works, what types of film succeed and what you can do to improve your film’s chances of profitability.

If you’ve got this far in the article and want a discount code, email me and I’ll send you one.

Further reading

In the meantime, here are some past research projects which can continue the journey right now:

- How movies make money: $100m+ Hollywood blockbusters

- How films make money pt2: $30m-$100m movies

- How is a cinema’s box office income distributed?

- There’s much more about horror films in my 200+ page Horror Report

- What types of low-budget films make the most money?

- Patterns among the most profitable movies budgeted $3m to $10m

- Patterns among the most profitable movies budgeted $10m to $20m

- Patterns among the most profitable movies budgeted $20m to $50m

- Do BFI backed films make a profit?

- Full costs and income of a $1m independent feature film

Notes

The data in today’s article covers live-action fiction films (i.e. not documentaries or animations) which were first released to the public between 1st January 1999 and 31st December 2018. The raw data came from a large number of sources, mostly public but a few from industry friends. I’m very grateful to everyone who has helped me with this, whether they’ve given me data, advice or just support.

The data in today’s article covers live-action fiction films (i.e. not documentaries or animations) which were first released to the public between 1st January 1999 and 31st December 2018. The raw data came from a large number of sources, mostly public but a few from industry friends. I’m very grateful to everyone who has helped me with this, whether they’ve given me data, advice or just support.

I’ve defined ‘independent’ as meaning not made or released by a major Hollywood studio. This includes a small number of big-budgeted films, which some filmmakers may not feel represent their experience. In any broad criteria, there will be subjective lines drawn over what to include and this feels the least egregious of the available options. I have defined “theatrical release” as at least $1 of reported gross in Domestic (i.e. USA and Canada) cinemas. This is a slightly tougher measure than just saying it was “in cinemas” as it removes the vanity release for awards etc at which no-one shows.

A film being “profitable” and its investors receiving all their money back are (sadly) not synonymous. My calculations estimate the likely net profit to the producer after all income and all costs are taken into account. However, if the film has struck an unfavourable deal with any of the third parties, or if the investors are not repaid pari passu from first dollar producers net profit, they could still be left out of pocket. Conversely, an investor who has their investment first in the recoupment waterfall could be quids in before others have been made whole.

Any model which looks at a whole sector will involve some generalities. For the vast majority of films, I do not have a final figure on the exact amount of money the producers made and so have applied formulae and rules of thumb to the data I do have. This is going to be harder to do in the future, as VOD becomes an ever-bigger part of the film value chain and if Netflix et al don’t suddenly start releasing more financial data (don’t hold your breath!). This is bad news for filmmakers as it makes it harder to predict how much a film might recoup and harder to know your film’s true market value when presented with an offer.

This also undercounts those movies which get significant income from non-traditional sources. These could include:

- Crowdfunding the initial budget, meaning there is far less (or maybe nothing) to repay.

- Private communities, such as religious organisations, online groups or hobbyists.

- Films which earn large amounts from VOD platforms despite not getting a theatrical release (i.e. films funded by Netflix).

- Income from merchandising, music sales and spin-offs. These are extremely rare among independent films. An example would be the micro-budget film Once, which spawned successful albums and even a Broadway show.

My research into the sector suggests that the above comprise a very small number of titles and do not shift the big picture shown today.

Studios do make films which are not for cinemas (a.k.a. “straight-to-video”) but they were not included in today’s research as I am only looking at films intended for theatrical release. I am using the same rough criteria as the British Film Institute (BFI) which defines a feature film as a film ‘intended for theatrical release’ and does not look to assess the likelihood of such a release. Unlike the BFI, I have added a length criterion, including only films which run at 70 minutes or longer.

In the first version of this article, I mischaracterised the Opus Data film catalog due to a misunderstanding my part. I’ve been happy to correct the topic and many apologies to those involved for the error.

Epilogue

My research into the film industry has never really been guided. I’ve investigated topics as they’ve occurred to me, as they’ve been requested by readers and as I learned new methods of data gathering and crunching

Over the past couple of years, however, I have started to feel that my research is building towards a bigger project: to zoom out and assess the whole film sector. I’m far from finished, but this profitability project is a big milestone for me in trying to fully understand how the film world works.

I’m really excited to be able to share it with filmmakers – both here on the blog and at live events around the world. I will be taking to the road to run training events whenever there are filmmakers who need help.

If you feel your town or community could benefit from this, drop me a line, especially if you run an organisation that can help with logistics and promotion in your area.

Comments

i have a question — if it doesn’t go to theatres is it really a movie. its a failed movie

Hi Don. That’s one way of looking at it. As with any study like this, there are subjective decisions made along the way. You could take a view that a movie becomes a movie when it’s creators intend it to be one, or at the other end of the spectrum, you could take the view you hold which is that it’s the film’s final outcome which defines its legitimacy. There is no one right answer.

It’s certainly become a lot harder to tell than in the previous century when you could largely group films into three categories – Movies (which played in cinemas first), TV movies (which looked like a movie but premiered on TV channels) and Straight-to-video (which had their first outing on VHS/DVD). Today there are many complicating factors which make this much harder, including:

1. There are far more types of movies (i.e. Netflix movie, four-walls tiny releases, etc)

2. There is much more blurring of the lines (i.e. simultaneous releases, Netflix movies which play briefly in cinemas such as The Irishman, etc)

3. There is far more acceptance of movies which don’t reach cinemas (i.e. Bird Box etc)

4. It’s so much easier to make a movie that the previous barriers to entry are gone. Just getting enough film stock to shoot a 90-minute movie was expensive (let alone the other costs) and so there were fewer movies but those that did get made were easier to spot as movies. Today there are YouTubers making long-form content with high production values and many millions watching their work.

So every organisation is forced to make their own call about what they regard as a movie. Major newspapers used to commit to reviewing every movie which reached cinemas but that’s just not possible now so they have to start refining their rules. It’s harder when there is money at stake, such as tax breaks, or the value of a future TV deal is linked to getting a cinema release.

I honestly don’t know what this question will look like in ten years time. The fragmentation of classification is a natural process when a market grows and changes, but it makes data research much harder!

I wonder what proportion of those who didn’t get a theatrical release expected or hoped to get one (if they’d even admit to it). 90.3 percent is a striking figure, but, as you’ve mentioned, digital technology lowers the barriers to entry, flooding the market, and new distribution channels mean cinema is not the holy grail it once was. If they never planned to get a cinema release, they couldn’t be called failures, though I’m sure a lot of those statistics in unreleased band represent genuine disappointments for some of the people involved.

(I write while in post-production on my first feature as a driector, with every hope we will get a theatrical release somewhere one day.)

Thank you for this great work!! Can you share the data?

Hi Kevin.

I’m afraid not, for a few reasons. Mostly because this methodology is fine for sampling the general shape of a large marketplace but would not hold up for individual films. There are always outliers, exceptions and unexpected results. For individual films you’d need to research each of its releases in far more detail than I did.

The other reason is that I don’t want to start declaring how much movies made from the outside as this could cause serious problems for those involved. If I’m wrong, then people could think they are owed profits they’re not, and even if I were somehow exactly spot on, the exact terms of their distribution deals may have meant that a different total actually reached the producers.

Thank you for all the hard work you do for the film community.

Do Netflix movies make a profit and if they do how much?

Thank you!

Hi David. It’s really hard to tell because the business model is fundamentally different from the indie filmmaking world. Early Netflix deals seem to have been pick-ups of finished or almost-finished films, whereas the newer ones are commissions (more akin to a TV deal). Their data is kept extremely private and the lack of releasing on other platform leaves us without a way of modelling the level of success the film made have had.

This is a really interesting study, thanks Stephen! I think it’s worth mentioning, that in this day and age of VOD and streaming, while theatrical release is desirable, if a film does not have a theatrical release, it doesn’t necessarily mean that it’s a ‘failure’ or that it didn’t do well in terms of distribution. A side note from this article, but these conclusions shouldn’t be a deterrent for independent filmmakers! 🙂 Thanks again for your work, I love reading your research and findings.

There is a flip side to this as well I believe. I think we have all probably been to festivals where we saw something that we really like yet for some reason was never picked up. I always wondered if there was a way now that the platform connect exists where these “Failed” films could be curated and presented a way that people would gain trust in for picking good pieces.

Hi Dimitrios

It’s a good point. One of the things I am always seeking to understand is the efficiency of the film industry. At times, I think it’s actually quite open and good at finding good/commercial films, no matter their source. Evidence for this would be films like Paranormal Activity or films coming out of festivals or foreign countries to do well globally. By then other times you experience exactly what you noted, i.e. see a gem at the festival which is largely ignored and you start to think that it’s all who you know.

There’s no doubt there’s an element of both. Currently, I’m more in the former, with everyone knowing the potential of a breakout hit made/acquired for low cost but I’m sure many good films slip through the net.

I’d say there are a few factors to contend with:

1. The volume of films made and even shown at festivals is large. Talk to any festival programmer and they will attest to the mammoth job of finding films for their programme. And that’s just one festival in one year. If you’re looking for ignored gems then almost any film made could be a potential pick-up, meaning you couldn’t even do any filtering (which is what producers do when they say a script has to come through an agent, for example).

2. Films need marketing to build an expectation and to attract the right audience. It’s an expensive business which is very hard to scale.

3. Audiences are lazy. I know – I’m one of them! Few are keen to hunt around for the perfect gem and would rather settle for whatever Amazon, Netflix or the multiplex will offer them. And this isn’t because they’re bad people (well, not all of them) but rather than they have lives/pressure and want an easy way to relax. Think about how you shop in the supermarket – do you really want to search harder for a slightly better apple? Most people don’t.

That’s not to say why such a platform couldn’t happen, just explaining possible reasons why one hasn’t become big thus far.

This was a depressing and enlightening article. In the comments I saw that some noted that a festival film well received even commercial and very genre can through lack of marketing money or a bad deal or just bad luck can get lost and I am living that. My team of crazy talented crew and cast made my film with me and we created a great little b-movie noir film set in the ’40s and its jst not been able to find an audience no matter my long and extensive albeit funding scarce posting and social media and hustle. Sometimes the world isn’t ready for what you have to offer, or it isnt well received or no matter how entertaining it gets lost. It’s heartbreaking.

Hi Stephen,

This is great! Are you a horror film fan?

Now you have me wondering what the data looks like on these three issues:

1) How does nudity/sexual content affect profitability (non-pornographic)?

2) How does voilence affect profitability?

3) How does MPAA rating affect profitability?

Keep up the fantastic and engaging work!

Best, Jeff

Oof, these are great questions that I would love to see the answer to.

Are these covered in your comprehensive Horror Report? I’ve been meaning to buy that!

Hi Stephen

Thanks for the laborious effort and the wonderful article.

I have a feature length documentary film coming out soon. No other investors. My subjects are two mostly unknown people who have lived spectacularly intertwined lives.

I doubt it would get any major distribution but numerous smaller distributors were interested in the story at AFM (American Film Market).

Do you have data on docs I could read?

Thank you again

Martin McGuire – Writer/Producer/Director of “Never Say I Can’t” a documentary film

Hi Martin

I’ve not studied docs in a lot of detail, I’m afraid. I’m starting to, so hopefully in the coming year or so I’ll be able to share more about them.

My son is taking a film class in college and he wants to make his own independent film! It’s helpful that you said to look at the whole market because that’ll give you an idea of which films make the most money, as you mentioned. It’s important that he makes profit from the movie he makes because he’s spending a lot of time and money to make it.

Stephen, If i were to give you the link to my not yet released action adventure science fiction feature film Warrior http://www.themoviewarrior.com, would you be able to and would you provide me with a projection of the revenue generated from its worldwide distribution for theatrical exhibition, television network telecast, digital platform and DVD sales for home entertainment? Bruce Singman brucesingman82@gmail.com 310 486-0995 http://www.brucesingmanesq.wordpress.com

How many people are actually able to live off of production? and how high are the percentages of having a successful movie being a small producer?

I’m confused, baffled really, by the assumption that everyone is seeking theatrical?! I didn’t direct my first movie thinking that would be the case. I won’t do my second that way, either. The producers I work with make movies with the biggest names in Hollywood, yet hardly any of those films had a substantial theatrical release. They’ve been doing this for 30+ years, producing for 20 of those, it’s not spectacularly hard to turn a profit on movies in the $1M to $10M range, there are lots of avenues for that and direct sales can mean quick recoupment. They wouldn’t still be doing this if they lost money every time out, yet their movies are on Hulu, Netflix, etc.

Hi Jonathan

It’s certainly something that’s changing over time. In the far distant past, we had the spectres of “Straight to Video” and “TV Movie” which many filmmakers would turn their noses up at. As TV has got better, budgets increased and now with major money going into streaming, things are changing. Plus there are more channels than ever to reach audiences. The article was written pre-pandemic, at which point the vast, vast majority of filmmakers I spoke to were hoping for theatrical release to kick of their journey to market. I’m not sure how things have shifted since but I would have thought there is a much more flexible outlook to their thinking.